Course Content

1.

Accuracy Score

0 min

2 min

0

2.

Activation Function

0 min

2 min

0

3.

Algorithm

0 min

2 min

0

4.

Assignment Operator (Python)

0 min

2 min

0

5.

Artificial General Intelligence (AGI)

0 min

3 min

0

6.

Artificial Intelligence

0 min

4 min

0

7.

Artificial Narrow Intelligence (ANI)

0 min

3 min

0

8.

Artificial Neural Network (ANN)

0 min

2 min

0

9.

Backpropagation

0 min

2 min

0

10.

Bias

0 min

2 min

0

11.

Bias-Variance Tradeoff

0 min

2 min

0

12.

Big Data

0 min

2 min

0

13.

Business Analyst (BA)

0 min

2 min

0

14.

Business Analytics (BA)

0 min

2 min

0

15.

Business Intelligence (BI)

0 min

1 min

0

16.

Categorical Variable

0 min

1 min

0

17.

Clustering

0 min

2 min

0

18.

Command Line

0 min

1 min

0

19.

Computer Vision

0 min

2 min

0

20.

Continuous Variable

0 min

1 min

0

21.

Cost Function

0 min

2 min

0

22.

Cross-Validation

0 min

2 min

0

23.

Data Analysis

0 min

7 min

0

24.

Data Analyst

0 min

4 min

0

25.

Data Science

0 min

1 min

0

26.

Data Scientist

0 min

6 min

0

27.

Early Stopping

0 min

2 min

0

28.

Exploratory Data Analysis (EDA)

0 min

2 min

0

29.

False Negative

0 min

1 min

0

30.

False Positive

0 min

1 min

0

31.

Google Colaboratory

0 min

2 min

0

32.

Gradient Descent

0 min

2 min

0

33.

Hidden Layer

0 min

2 min

0

34.

Hyperparameter

0 min

2 min

0

35.

Image Recognition

0 min

2 min

0

36.

Imputation

0 min

2 min

0

37.

K-fold Cross Validation

0 min

2 min

0

38.

K-Means Clustering

0 min

2 min

0

39.

Linear Regression

0 min

2 min

0

40.

Logistic Regression

0 min

1 min

0

41.

Machine Learning Engineer (MLE)

0 min

5 min

0

42.

Mean

0 min

2 min

0

43.

Neural Network

0 min

2 min

0

44.

Notebook

0 min

3 min

0

45.

One-Hot Encoding

0 min

2 min

0

46.

Operand

0 min

1 min

0

47.

Operator (Python)

0 min

1 min

0

48.

Print Function (Python)

0 min

1 min

0

49.

Python

0 min

5 min

0

50.

Quantile

0 min

1 min

0

51.

Quartile

0 min

1 min

0

52.

Random Forest

0 min

2 min

0

53.

Recall

0 min

2 min

0

54.

Scalar

0 min

2 min

0

55.

Snake Case

0 min

1 min

0

56.

T-distribution

0 min

2 min

0

57.

T-test

0 min

2 min

0

58.

Tableau

0 min

2 min

0

59.

Target

0 min

1 min

0

60.

Tensor

0 min

2 min

0

61.

Tensor Processing Unit (TPU)

0 min

2 min

0

62.

TensorBoard

0 min

2 min

0

63.

TensorFlow

0 min

2 min

0

64.

Test Loss

0 min

2 min

0

65.

Time Series

0 min

2 min

0

66.

Time Series Data

0 min

2 min

0

67.

Test Set

0 min

2 min

0

68.

Tokenization

0 min

2 min

0

69.

Train Test Split

0 min

2 min

0

70.

Training Loss

0 min

2 min

0

71.

Training Set

0 min

2 min

0

72.

Transfer Learning

0 min

2 min

0

73.

True Negative (TN)

0 min

1 min

0

74.

True Positive (TP)

0 min

1 min

0

75.

Type I Error

0 min

2 min

0

76.

Type II Error

0 min

2 min

0

77.

Underfitting

0 min

2 min

0

78.

Undersampling

0 min

2 min

0

79.

Univariate Analysis

0 min

2 min

0

80.

Unstructured Data

0 min

2 min

0

81.

Unsupervised Learning

0 min

2 min

0

82.

Validation

0 min

2 min

0

83.

Validation Loss

0 min

1 min

0

84.

Vanishing Gradient Problem

0 min

2 min

0

85.

Validation Set

0 min

2 min

0

86.

Variable (Python)

0 min

1 min

0

87.

Variable Importances

0 min

2 min

0

88.

Variance

0 min

2 min

0

89.

Variational Autoencoder (VAE)

0 min

2 min

0

90.

Weight

0 min

1 min

0

91.

Word Embedding

0 min

2 min

0

92.

X Variable

0 min

2 min

0

93.

Y Variable

0 min

2 min

0

94.

Z-Score

0 min

1 min

0

- Save

- Run All Cells

- Clear All Output

- Runtime

- Download

- Difficulty Rating

Loading Runtime

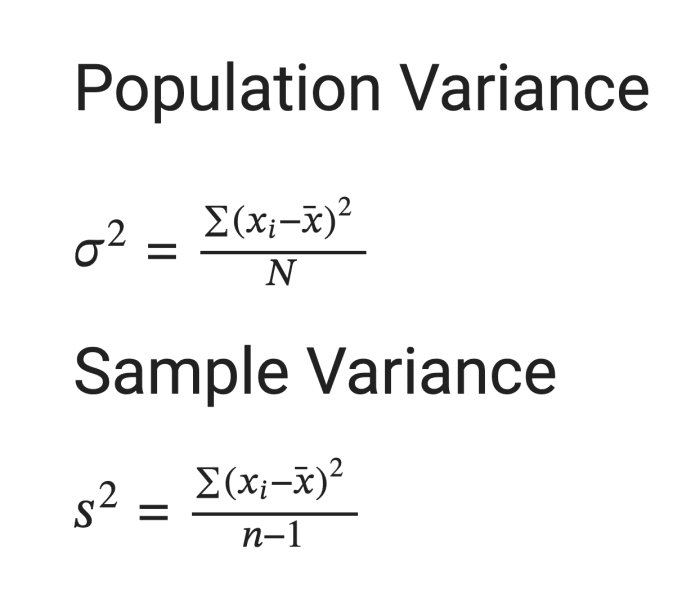

In statistics, variance is a measure of the spread or dispersion of a set of values. It quantifies how much individual data points in a dataset deviate from the mean (average) of the dataset. In other words, it provides a numerical measure of how scattered the data points are around the mean.

Key points about variance:

- Squared Differences: Variance involves squaring the differences between each data point and the mean. This squaring ensures that both positive and negative differences contribute to the overall measure of dispersion, and it amplifies the impact of larger deviations.

- Units: The variance is expressed in the square of the units of the original data. For example, if the data represents lengths in meters, the variance will be in square meters.

- Low Variance vs. High Variance: Low variance indicates that the data points tend to be close to the mean, suggesting a more concentrated or tightly clustered dataset. High variance suggests that the data points are more spread out from the mean, indicating greater variability or dispersion in the dataset.

- Standard Deviation: The square root of the variance is called the standard deviation (σ). It is often used as a more interpretable measure of dispersion because it is in the same units as the original data.

Variance is a fundamental concept in statistics and plays a crucial role in understanding the characteristics of a dataset. It is used in various statistical analyses and is a key component in the calculation of standard deviation and other measures of variability.